Cisco Systems Inc. (CSCO) is one of the largest networking hardware and software provider in the world. It also started giving out dividends in 2011. I wanted to analyze the safety of the CSCO dividend and look at its future prospects. We will do an overview of what Cisco Systems does and then look at its financials.

Overview of Cisco Systems Inc.

Cisco Systems Inc. (CSCO) is large cap American multinational company that focuses on building hardware/software related to computer networking, security, applications & collaboration in cloud and on-premise environments. Think of them as someone in business of building infrastructure to help world of internet function & grow. They mostly build these tools and services for enterprise customers. You might go and buy a Wi-Fi router or modem to allow you to tap into internet connection provided by your ISP. Most big business need to do this but, at a much larger scale. Most companies have their own data center. They usually setup their own private internet which employees work on. This needs to be done across multiple sites across multiple countries. They need to make sure connection is secure and only legitimate employees can connect. Employees use various devices. Companies need to make sure employees can connect using these devices from workplace or while travelling etc. The complexity involved with so many factors is huge. Cisco essentially provides their own proprietary hardware/software to help business manage their users, devices etc. connect to their own network and the global internet in a secure manner.

CSCO in Cloud Era

However, times are changing. Cloud is the new jargon. Nearly every big company on earth is looking at implementing or has implemented some or the other cloud-based applications/solutions. Most big cloud providers like Amazon, Google & Microsoft do not use Cisco switches or hardware in their data centers. They prefer to use white box(open source) cheaper alternatives to do networking. Companies today are preferring to outsource infrastructure/networking/storage related tasks to these cloud providers. This gives them even more money/effort to focus on their core competency. So, this can represent a challenge to Cisco for future growth.

Software Defined Networking (SDN)

What is making it possible for public cloud providers to use white box hardware instead of Cisco’s hardware? A new software based approach to manage networks. Traditionally the data plane (responsible for moving data across hardware) & control plane (responsible for controlling flow) used to reside within the hardware itself. Changes in config had to be done physically at the device and by a human. However SDN separates the logic from data flow. You can now make any changes using software. The actual hardware switch/router will act on them. So, this leads to easy reconfiguration of hardware using software. Now the hardware can be by any company and the software is what matters. This is a big shift in networking industry.

courtesy researchgate (click/hover to remove caption)

I work on the IT programming side for a big company. I can safely say that not all applications are going to be moving to cloud anytime soon. Hence, you have a situation where 15-20% of the applications are in a public cloud, some in private cloud and rest are still on their own on-premise data centers. Moreover, cloud applications are also distributed among various providers like AWS, Azure, Google etc. I can already see we work with AWS, Azure, Oracle cloud products on top of managing our own data center. We now have requirements to make sure one application residing in one cloud can communicate with some other application in our private data center or some other cloud. This type of setup is known as a multi-cloud environment.

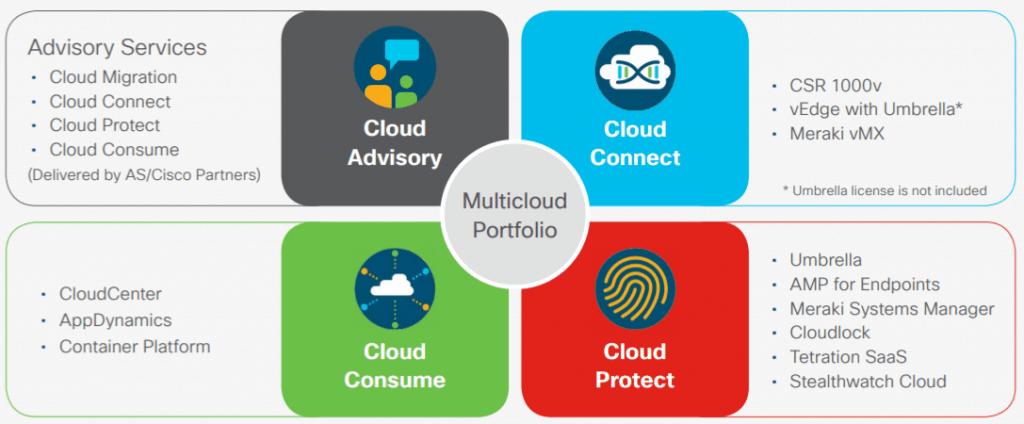

An Exciting Opportunity

Imagine the amount of challenges this will have across multiple applications/platforms/users for networking and providing a seamless user experience. Cisco is already positioning itself as the leader in this multi-cloud space. They are now creating more software to manage networking and communications between multiple cloud environments. Here are some examples of their products:

| Domain | Product | Competitor |

| Infrastructure-switches | Catalyst 9000 switches with Cisco DNA software | Arista Networks, Huawei, HP |

| Infrastructure-routing | SD-WAN with Cisco DNA | Juniper, Riverbed, Alcatel Lucent, Fortinet |

| Infrastructure-wireless | Catalyst and Meraki based wireless access points | HP, Ubiquiti, Extreme Networks |

| Application-collaboration | Webex, Cisco telepresence | Microsoft, Zoom, Slack |

| Application-analytics | AppDynamics | New Relic, Dynatrace |

| Security-endpoint | AMP, Any connect VPN, Umbrella | Fire Eye, Citrix, Zscaler, Fortinet |

| Security-cloud | Cloud email security, stealth watch cloud etc. | Palo Alto Networks, Fire Eye, Symantec |

I am sure I have probably missed many other Cisco applications in the above table. But Cisco has some or the other cloud feature for each of the above apps/hardware.

They can either be found on app stores of biggest cloud providers or can be used as SaaS solution from Cisco themselves. Cisco is aggressively converting many of their hardware contracts by providing some cloud software to manage the underlying hardware. Again, this has been possible after moving logic and hardware into different layers in first diagram. Software to manage networking hardware and security is becoming more important. Then bundling this as subscription-based solution instead of customers buying the hardware & paying a one-time fee. Historically, Cisco has been a bit cyclical and there is some drop off revenues after every few years. But by moving into subscription style sales, they will address this in few years.

Cisco Systems seems to be on right path

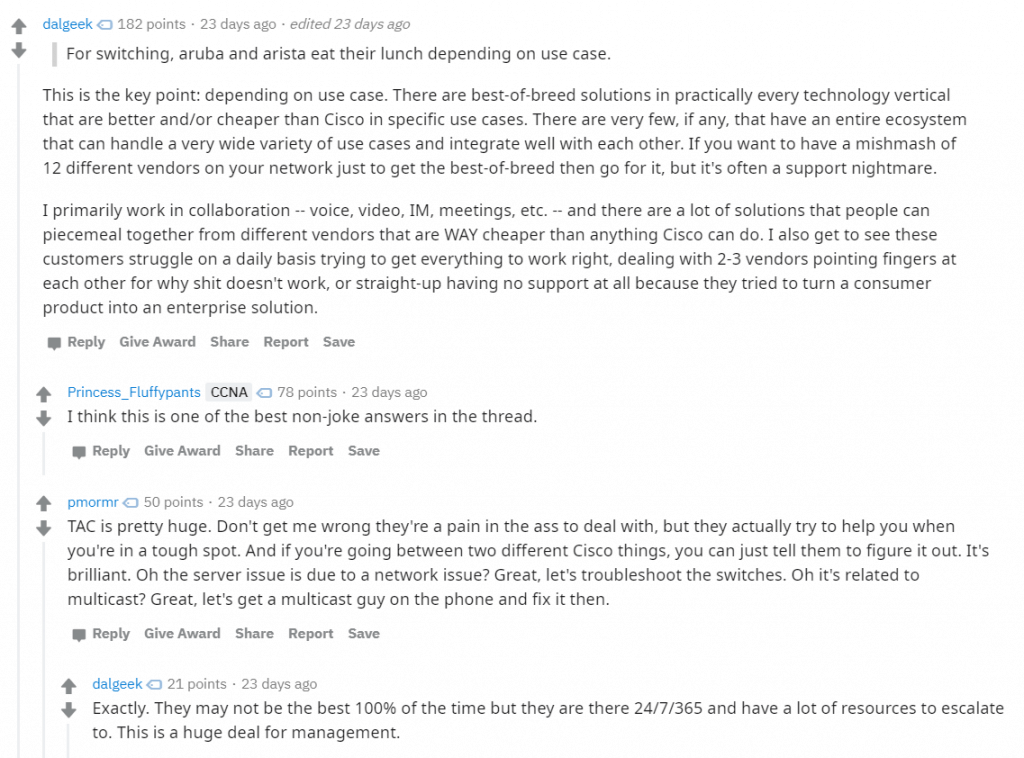

Cisco provides application/hardware over most networking sub-categories. They do not have to be the best at everything or even one thing. Most of their products are in top 3-4 in every category. That is all they need. For any business looking for their networking needs for multi-cloud, Cisco can probably cater to everything. Provide support for everything under one roof. That is a big usp for most of their customers. Being in similar position at my job, I realize support is very important. If one company can provide me support for multiple solutions, I would like that instead of chasing customer support for 2-3 different vendors. Its not just me saying this, check out a post from reddit where multiple system and network admins talk how important support is in big companies:

Point is, it seems like Cisco is again trying to become one stop shop for everything you would need to manage multi-cloud environment at any enterprise. Cloud is immense opportunity to grow, has lots of challenges and Cisco Systems seems to be well equipped in all fronts.

Cisco Silicon One

On 12th Dec 2019, Cisco Systems announced it was getting into the business of selling chips. Historically, Cisco has been making and designing its own chips that go into its routers and switches. However, only way to get them was by using Cisco’s own hardware. As I mentioned above with increasing adoption of cloud, Cisco had not been able to sell its hardware to Google, Microsoft, Amazon or any big cloud provider. However, white box chips/hardware needs a lot of R&D and investment. Cisco Systems is now starting to sell these chips to any customer who wants them separately. They will do the R&D and make chips that will work in any white box router, switch or other networking hardware and design it to be more efficient. This move really helps them to start selling to these big cloud providers I mentioned above. Its a completely new business line for Cisco Systems and brings them in competition with Broadcom, Juniper which used to have their chips in this white box hardware so far.

Financials (Cisco Systems)

Here is a financial snapshot from Valueline with last 15 year results:

courtesy ValueLine (click/hover to remove caption)

Revenues

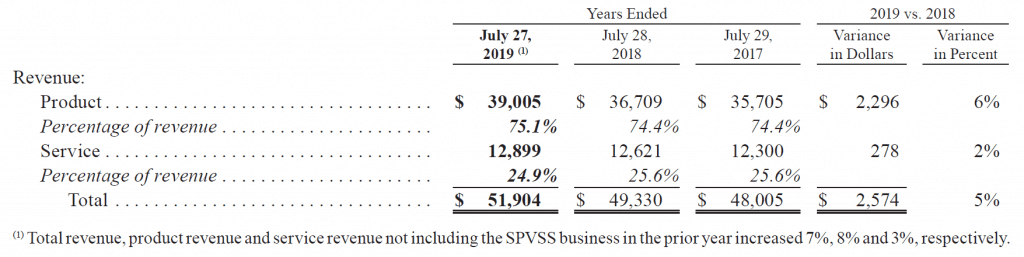

It is important to note that CSCO’s fiscal year lasts from Aug-July of every year. Keeping that in mind, in recently concluded Year 2019 in July, CSCO made about 51.9 billion in revenues. This was 5% growth as compared to fiscal 2018. Services grew by 2% and products revenue by about 6%.

If we look at revenues by different segments Cisco operates in:

Security is going to be massive in the multi-cloud world. So Cisco growing 16% in that and another 15% in cloud applications segment is great to see. Switching and Router products come under the infrastructure platforms which also grew by 7%. This segment is most challenged by SDN and good to see that Cisco grew revenues in this segment. I think this is where they are probably bundling some controller UI or software to manage routers and switches. So Cisco is already on the offensive to make sure they remain relevant in multi-cloud world.

However, in Q1 2020 ending in Oct 2019, CSCO only had a 1% increase in revenue and guided down to -4% revenues in Q2 2020. They attributed this to the weak macro environment. With Brexit and trade war between US and China still unresolved, its possible many of its customers are holding back on investing in networking equipment. Additionally, most telecoms are currently only using 4g equipment to demo 5g networks. So, less revenue on that side as well. Another reason might also be them converting one-time payments customers made, into deferred revenue subscription model. So, upfront revenue would be less as compared to previous years. But, it will be realized over the life of the contracts (multiple years).

Dividend Yield & Safety of CSCO Dividend

| Dividend per share as of Nov 2019 | $1.4 |

| Price as of Nov 22 2019 | $44.85 |

| Dividend Yield as of Nov 22 2019 | 3.12% |

| EPS as of Jul 2019 | $2.61 |

| EPS Payout Ratio as of Jul 2019 | .5363 or 53% |

| Cash flow per share as of Jul 2019 | 14.922/4.273 billions = 3.49 |

| Cash flow Payout ratio as of Jul 2019 | (1.4/3.49)=40.11% |

| 9-year DGR | 23.02% |

| 5-year DGR | 13.146% |

| Latest dividend increase in 2019 | 6.06% |

Cisco Systems pays a 1.4$ dividend annually at 3.12% yield as of Nov 2019. Moreover, the payout ratio based on eps and free cash flow both seem relatively safe as compared to other tech companies. I think Cisco has some wiggle room during this period of transiting their business to cloud and subscription base. Looking at the latest dividend increase of 6% and the 9-year average of 23%, it looks like CSCO has tempered down their raises a bit. Although, I am still expecting mid to high single digit raises going forward. 3% starting yield with 6-9% yearly increases can still help return about 10% return on dividend income every year which is great!

Ability to Service Debt and continue paying dividend

| Total Debt at end of fiscal 2019 | $24666 million |

| Total shareholders equity at end of fiscal 2019 | $33571 million |

| Debt/Equity | 24666/33571 = .734 or 73% |

| Operating Income as of end of fiscal 2019 | $14219 million |

| Annual Interest payments | $859 million |

| Interest Coverage ratio | 14219/859=16.55 |

Cisco’s competitors have a lower d/e ratio. JNPR is at 40, ANET is at 3% & HPE is at 59%. Cisco is a highly acquisitive company. Here is a list of about 200+ acquisitions they have made since 1984. I think they’re just being very opportunistic in such a low interest rate environment. Making smart acquisitions and with a huge history, making those work. Having a interest coverage ratio of 16 means they have enough earnings to pay interests and service their debt. Cisco generates a lot of cash even after dividends and can pay debt down if it wanted to within 3 years. Thus, having debt/equity ratio a bit on the high side shouldn’t be much of a problem for a cash cow like Cisco Systems.

Trends

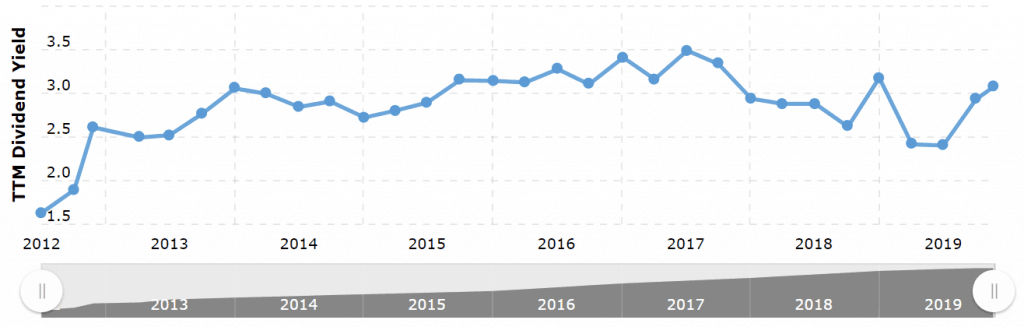

There is a very popular reversion to mean theory. It says that most stock metrics tend to hover around the mean of its lifetime average. So if the PE of a stock increases to very over-valued, over time it will fall back to its mean PE ratio. Hence, I also like to look at average PE ratio and dividend yield of stock I am looking to purchase as compared to its historical values. This plays a small part in my decision-making process. Cisco only started paying dividends 8 years back in 2011. Using Macrotrends, we can see the current yield of 3.12% is higher than the overall average yield of 2.67% over 9 years.

The fwd pe ratio as of Nov 2019 is 13.77. Average annual PE over last 11 years is about 13.37. Ignore the spike in 2018, its from tax reforms and them paying taxes to bring cash back into USA.

As you can see both pe ratio and dividend yield seem higher or close to the average in last 9-11 years.

Risks

Cloud

As mentioned earlier, Cisco faces threat to its core hardware business which made more than 50% of it revenue in 2019. With more enterprises looking to move applications to cloud to reduce operational costs, less Cisco hardware gets purchased. But with Cisco trying to move to more subscription based business and getting into chip selling business, I think they are moving in right direction. Move to cloud is definitely happening but it will take time and till then we will be in a multi cloud environment for which Cisco seems well prepared.

Trade War

Cisco’s sales in China fell a whopping 26% from the 2018. Just as US is trying to eliminate Huawei equipment from its upcoming 5G network, Chinese government is making sure it avoids equipment from US based vendors. Although Chinese sales only comprise of about 3% of overall revenues for Cisco. However this could be a long term trend. Secondly impact of tariffs on Chinese goods also increases price of Cisco hardware coming into the US. So at least a resolution in trade war could help Cisco on one of these issues.

In Conclusion

Cisco in its most recent fiscal Q1 2020 guided revenues to be down in its fiscal Q2 by about 3-5%. They attribute it to their slowdown of sales in China, general macroeconomic environment and less investment in buying products by cable & telecom companies. With 5g standards still being finalized, slowdown in cable and telecom industries can be explained. Trade war can explain slowdown in sales in China and rest of the world as many customers seem to be delaying investments in technology improvements. They want to wait and watch because of the uncertainties. Eventually, 5g will be here. Companies won’t be able to keep delaying investments in upgrading their networking and cloud infrastructures. ANET & JNPR have both given lower guidance between SEP-NOV 2019. So, it does look like this is a broad industry issue and not just CSCO doing something wrong. The macro economic weakness may go on for a few quarters. But, Cisco Systems CEO Robbins did mention they expect fiscal Q1 2021 to be better.

In the meanwhile, we get a cash cow paying 3+% safe yield and maybe even growing it mid-high single digits every year. This could be a good time to at least start a position for the long term in a tech stock that pays dividends. I am long CSCO.

Please check out my complete dividend portfolio and analysis of other dividend stocks.

I am by no means an expert on networking technology. So, I will also love to hear your opinion on the analysis in the comments below. Is Cisco Systems on the right path on the way to Cloud future?

References:

Disclaimer: The above are just my opinions expressed in the article. I am not your fiduciary or an investment advisor. Do not consider this as investment advice to you. This article is just for informational and entertainment purposes. Also please note that this article was published on Nov 26th. Many numbers would have changed when you are reading it.