Since many of you know dividend investing is one of my fav styles of investing. I wanted to start a new series of articles on dividend stocks. I plan to discuss fundamentals of the business I am buying, some very basic technical metrics to judge safety of dividend over long term. My plan on dividend investing is mostly to buy high quality companies at decent or undervalued prices. Focus more on the income that is being generated using dividends, re-invest and hold for the long term. These articles will also help me to revisit my theory on buying the stock in first place in future when deciding if ever to sell.

So without any other delays, a stock I have been looking at recently is BlackRock Inc.

Overview of BlackRock Inc (BLK)

BlackRock is one of the largest asset management firms in the world. Basically, they are responsible for managing over 6 trillion dollars in various types of assets like fixed income, stocks etc. World’s biggest universities hand over the keys to  their endowment funds to BlackRock to manage it and grow. World’s biggest companies ask Blackrock to manage their pensions funds and grow them. Some of the world’s biggest wealth funds, tax exempt institutions, charities etc. engage in services of BlackRock to manage their money. Blackrock in turn charges them fees to do it. Apart from this, they also own the iShares brand of etfs. If you want to do index investing but want more liquidity in selling and buying your shares, you would look towards ETFs. ETFs like IEMG (emerging markets), ITOT(Total US stock market), IVV(US S&P 500) are products of the Blackrock family. These cost almost nothing to make, all they do is package different individual stocks and sell them together as 1 security and collect some fees every year on it. They already have country specific, industry specific, dividends specific ETFs. ETFs inherently reduce risk since it allows you to diversify. and provide liquidity. They are very popular among all type of investors retail/institutional or individual. Blackrock is the largest ETF provider in the world!

their endowment funds to BlackRock to manage it and grow. World’s biggest companies ask Blackrock to manage their pensions funds and grow them. Some of the world’s biggest wealth funds, tax exempt institutions, charities etc. engage in services of BlackRock to manage their money. Blackrock in turn charges them fees to do it. Apart from this, they also own the iShares brand of etfs. If you want to do index investing but want more liquidity in selling and buying your shares, you would look towards ETFs. ETFs like IEMG (emerging markets), ITOT(Total US stock market), IVV(US S&P 500) are products of the Blackrock family. These cost almost nothing to make, all they do is package different individual stocks and sell them together as 1 security and collect some fees every year on it. They already have country specific, industry specific, dividends specific ETFs. ETFs inherently reduce risk since it allows you to diversify. and provide liquidity. They are very popular among all type of investors retail/institutional or individual. Blackrock is the largest ETF provider in the world!

Tollbooth in the investment world

All this makes Blackrock analogous to Visa and Mastercard in payments world. Just like Visa/Mastercard charge fee on any transaction done across the world using their cards, BlackRock charges fee to people holding their investment assets. They charge it every year! So its not like a one time transaction fee either. It’s like a toll booth on the superhighway of investing. Lots of people/institutions/retail clients invest in assets and some/most of them will use assets packaged by BlackRock and pay fees to hold them.

Best part is as the total assets under management grows for BlackRock, the more fee discounts they can offer to their clients thereby growing even more. The services Blackrock offers are also very sticky. An institutional client or a retail investor with significant portion of their wealth invested and managed by BlackRock is not going to sell everything and switch to a new provider just because someone else offered lower fee. I think BlackRock has excellent moat in form of its size and brand. They are one of the absolute go to places for big institutional clients looking to manage their money.

Dividend Yield

As of Oct 25 2018 is 3.31% with 12.52$ payout per share per year

Dividend history & Growth

BlackRock has a pretty good history of increasing and growing dividends every year since 2003 except for 2009 when they froze it. For 2009 I think companies can be excused if they had a pause in dividend growth because of the worldwide scenario going on at that time. They could have just cut the dividend in 09 but they decided to just freeze it. This seems to suggest me that the management is invested in growing and increasing dividends year over year. The dividend over last 5 years has grown around at 13.18%. Such growth rate is just great! What is there to not like about this history and growth rate?

Payout Ratio & Dividend Safety

Courtesy Valueline Inc.

Looking at the past 15 years of data from Valueline, we can identify the following about dividend safety:

| Dividend per share as of 2018 | $12.02 |

| EPS as of end of 2018 | $26.93 |

| EPS Payout ratio | (12.02/26.93)*100 = 44.63% |

| Cashflow per share as of 2018 | $29.08 |

| Cashflow Payout ratio | (12.02/29.08)*100 = 41.33% |

So with payout ratio in 40’s it seems like BLK makes enough money to cover dividends. This also allows BLK to withstand competition in race to 0 over commission fees. BLK has the scale and the money to innovate and take market share from other companies in its field.

| Total Debt as of end of 2018 | $6000 million |

| Total Shareholder’s equity as of end of 2018 | $32374 million |

| DEBT/Equity | .185 or 18% |

| Operating Income as of 2018 | $5531 million |

| Annual Interest payments | $175 million from Annual statement |

| Interest Coverage ratio | 5531/175 = 31.60 |

.18 or 18% debt to equity ratio tells us, Blackrock has not used much debt to finance its assets and growth. Its competitors like State Street is at .53 or 53% Northern Trust is at .34 or 34%. Interest coverage ratio of 31 suggests that BLK should have no problems paying its interest obligations every year. It generates enough money to cover them 31 times! This is a good spot to be in. In case of a crisis, BLK should be able to support its debt obligations which will allow it to ensure dividend is also paid there after.

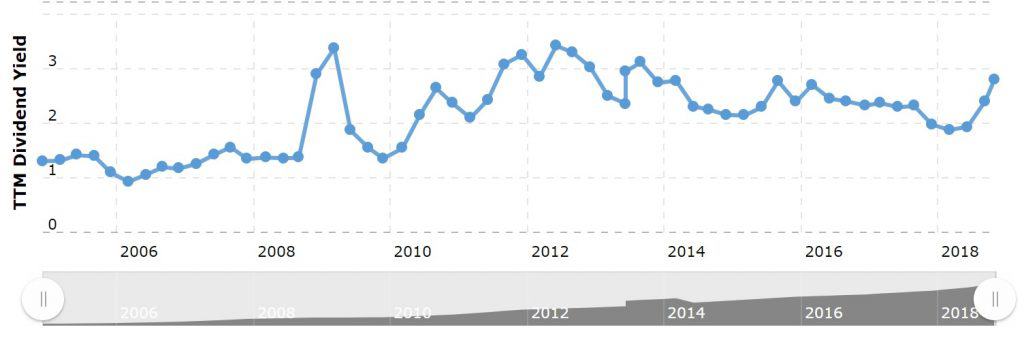

Trends

There is a very popular reversion to mean theory. It says that most stock metrics tend to hover around the mean of its lifetime average. So if the PE of a stock increases to very over-valued, over time it will fall back to its mean PE ratio. Hence, I also like to look at average PE ratio and dividend yield of stock I am looking to purchase as compared to its historical values. This plays a small part in my decision-making process. Looking at BLK historical PE, it’s been around 13-17. This chart below doesn’t include the latest price decline in month of October and including that, fwd pe today is around 12-13 PE. I think this is below the average in last 12 years.

Next coming up to the dividend yield, historically seems to range between 1.5 to 2.5%. Again, today the yield is close to 3.1%. Kind of the highest its been in last 12 years!

Looking at revenues and net income over the last 10 years from Morningstar shows us the following(in millions):

As you can see both revenue and net income have gone up in the correct direction over last 10 years. This just means management is great at growing the business and making it more efficient.

Positive trends tell us that BlackRock is just a great company that has reduced to reasonable levels in the last few months.

In Conclusion

BlackRock seems to be a fundamentally strong company with great dividend starting yield at around 3% at present. I usually only care about my dividend income and safety of that dividend. The dividend growth and payout ratio with BLK seems very good at current levels. I like to keep the whole process of picking dividend stocks simple and easy. Even if the stock drops more good for me since that means my DRIP will get more of BLK stock. If it goes up again good for me. I would just let the stock DRIP and reinvest all dividends. Usually I buy in lots and bought my first lot here. I will slowly buy more lots and build BLK into a full position for me over the next year or so.

If you liked this article, it will help us immensely if you can share it with your social circle.

Disclaimer: The above are just my opinions expressed in the article. I am not your fiduciary and not a financial advisor. Do not consider this as investment advice to you. This article is just for informational and entertainment purposes only. Please do your own research before making investment decisions or talk to a fiduciary.