Spin off’s present one of the most interesting opportunity for investing. They might have some irrational selling which will move the stock price downwards. Both Joel Greenblatt from Magic Formula Investing fame and Peter Lynch in One up on Wall Street mention to keep an eye on spin offs for best opportunities to invest. I believe there is something similar going on with Kontoor Brands, a recent spin off from VF Corp.

Allow me to introduce Kontoor Brands (KTB)

Kontoor Brands (KTB) is a newly created spin off from V.F Corporation (VFC). Its business is selling Wrangler, Lee, Rock & Republic jeans as well as operating VF Outlet business. VFC spun off this business in May 2019 to focus on their fast-growing adventure brands business. They wanted to focus more on them and decided to spin the jeans segment off as KTB. So Kontoor Brands started trading on 23rd May for about 40$ a share and then fell to about 26$ a share by June 25th.

Why did Kontoor Brands fall so much?

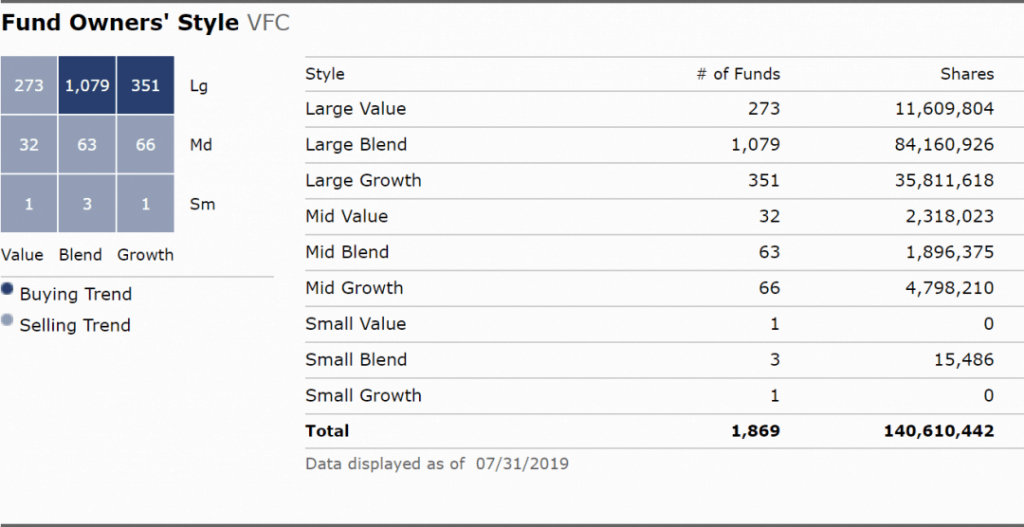

Irrational selling. Just like most big stocks, VFC had lots of institutional owners of its stock. If you look at Morningstar’s ownership details tab for VFC, you will find a huge amount of Large cap/dividend growth-based funds holding VFC stock.

You can see above most funds are large cap based funds. When KTB was spun off and started trading, its market cap was about 2-2.5 billion dollars. It was not part of SP500, neither was it considered a large cap company, nor had they made any official dividend announcement. On the contrary, KTB was a very boring, small-mid cap, non SP500, high dividend yield company with not a fast growing dividend. These large caps, SP500 focused, or dividend growth funds, would have been forced to sell most/all of their KTB stock. Since the new KTB stock did not follow any rules set by the fund for their holdings. I think this is the prime reason KTB stock took a dive after beginning to trade as an individual company. You can also see huge volumes of buy, sells in the first few days when mostly funds were selling:

The daily volume is far less now, 3 months after the spin off:

Management seems great and very shareholder friendly

KTB management has been touting the dividend policy of the company. Even before the spin off, the management spoke about a very strong dividend policy. Focusing on dividends as a major factor in total shareholder return. They already said in their roadshow, they planned to maintain a 60% target payout ratio. They even mentioned they plan to initiate a 2.24$ per share dividend equaling about 5+% of their 40-42$ trading price when it was spun off. So, when the price kept falling and a dividend was not announced, investors became skeptic of the planned dividend. I believe this contributed to further falling of the price. However investor’s fears were disproved when KTB announced a 2.24$ dividend per share on July 23rd 2019. Yield around 7%+ as of close on Jul 23rd.

I think this really speaks about the quality of management. Management promised something and delivered! The dividend is always at discretion of the management and the board. Management could have reduced the 2.24$ payout they mentioned before the spin off. They could have kept it at 5% of 26-28$. However, they followed through and delivered on the 2.24$ amount as previously mentioned.

Most of the KTB management has come straight from their parent company. The CEO, CFO and VP of supply chain all worked for VF Corp before moving to KTB. I see this as a great sign and shows confidence of the leadership in Kontoor Brands.

Now let’s talk about financials

Revenues for Kontoor Brands have been decreasing over the past 3 years and was one of the reasons VFC wanted to spin off this division. Revenues have decreased from about 2.92 to 2.76 billion dollars since 2016. This was mainly due to challenges in NA over retailer bankruptcies (Sears in 2018), India demonetization and exiting business in Argentina. Management expects them to decrease to 2.5 billion dollars in 2019. But then from 2020 on wards they expect for revenues to start growing at low-mid single digit rate.

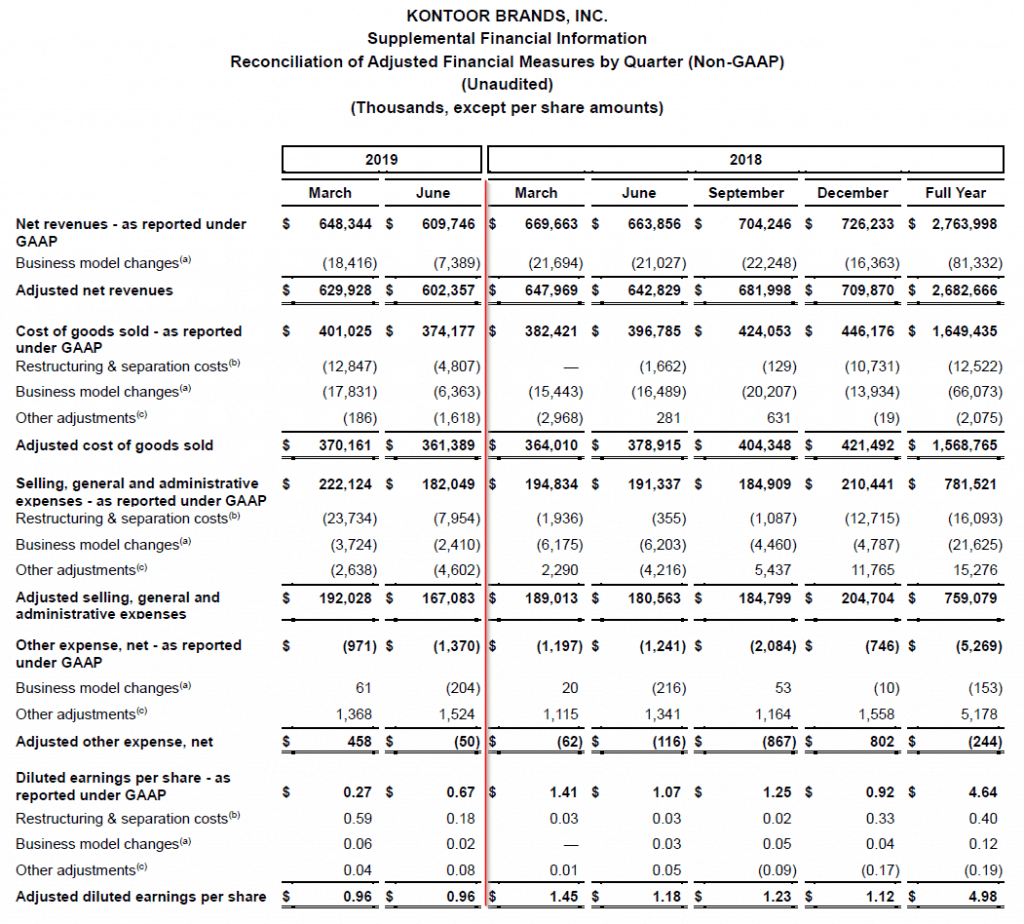

For the most recent Q2 2019 quarter, the adjusted EPS was .96$ a share. You can check out there Q2 earnings report right here.

The interesting thing you would notice is that they have the word adjusted mentioned at a lot of places. Adjusted EPS (0.96) is also higher than the GAAP EPS (0.67). But there is not much concern here. We need to remember that this is practically KTB’s first earnings report as an independent company. They are focusing a lot on restructuring currently. As part of Q2 2019, they ended up exiting business in Turkey & Argentina which were poorly performing. Changed business models to distribution from direct in Chile, Russia & Israel. Closing some factories in Mexico that used to produce goods for VFC.

All these steps cost money and KTB is excluding these costs and revenues from adjusted numbers as one time charges. They plan to continue investing in restructuring throughout 2021. This is kind of needed for a newly spun off company since this will eventually help them to cut a lot of costs which will reflect on the bottom-line soon. In fact KTB management expects to start seeing result from the restructuring program in second half of 2019 itself.

Current PE for KTB is 32.20/(.96*4) = 8.41 on an adjusted basis & 32.20/(.67*4) = 12.01 on GAAP basis.

Dividend Safety of Kontoor Brands (KTB)

According to adjusted EPS, payout ratio comes to be about .56/.96 = 58.3% for the quarter. According to GAAP EPS, payout ratio is .56/.67 = 83.5%. That’s a little high but as I mentioned, this reflects extra one time costs company has had to bear for restructuring. As we move forward into 2020 & beyond, cost savings will be realized and one should expect costs of operations to go down lower thereby improving the payout ratios on GAAP basis.

Based on free cash flow, its 53.39-9.3 = 44.09 Million in free cash flow. This results in (56.64*.56)/44.09 = 71% payout ratio on cash flow. Which is not bad at all and again this percentage should improve with the restructuring changes.

Interest Coverage ratio = GAAP EBIT / Annual interest payments which comes to about (52.15 *4)/60 million = 3.4 times. I annualized the 52.4 million EBIT to get the annual. On adjusted basis its (74*4)/60 million = 4.93 times.

This ratio just tells us if the company will have any extra money left after paying interest payments. Ideally 5 and over is better. I think on adjusted basis, KTB is almost there. On a GAAP basis they might take a couple of years to get there, but I am confident they will.

I expect all ratios mentioned above to improve with each passing quarter as Kontoor Brands management keeps executing on their restructuring plan. I will keep looking at their financials with each quarter to see if they improve or not.

Risks

Concentration of Revenues

Walmart accounts for about 33% of revenues in USA which is pretty huge considering they generate 73-80% of their total revenues in USA. In fact, 53% of revenues come only from 5 retailers in USA. So maintaining those relationships is very key to Kontoor Brands.

Lack of diversity

At the end of the day they mostly sell jeans. They do sell some shorts and some shirts, but most revenues are generated by the jeans segment.

Too much debt

As part of the spin off, 1 billion dollars in debt was taken out by KTB. That’s pretty huge. This is mostly long-term debt and company is in a very defensible industry selling jeans and related products. So the debt is a big concern with the juicy dividend yield. However only 20% of revenues in Q2 were from outside USA. So there is room for far more growth internationally where management said, they are now focusing. Lee is already number 1 jeans brand in China and KTB plans to introduce Wrangler in China in early 2020. Plus with all the operational efficiencies realizing over next 18-24 months, I can see the company focusing more on cash flow and bringing down the debt. They already paid off 50 million this quarter Q2 2019.

Still a new dividend company

Ideally most dividend investors like to look at multiple years of prior data. Dividend history, sustainability/safety, historical pe ratios etc. before making a decision on dividend stock. However KTB is still a very new company. They just declared their first dividend. So there is not much historical data to look at which might put off some investors.

Conclusion

Peter Lynch and Greenblatt do mention, special situations like spin offs create interesting opportunities to invest. They also mention there is huge imperative not just for the spun off company but also for the parent to see the spun off company succeed. If the spun off company fails it also reduces trust in the management of the parent company since it destroys shareholder value. VFC has always mentioned spin off will unlock lots of value for both companies and would allow KTB to focus more on gaining operational efficiencies and growing in jeans segment. This is just what KTB has been presenting and speaking about since day 1 of spin off.

I think KTB has been way irrationally oversold. The company has already declared dividends as they had been saying. They also have a good plan to achieve efficiencies in operations and cost. This is already showing signs of good management quality. They operate in a very boring but defensive jeans wear segment. They only had 11% drop in revenues during the recession. Management has mentioned multiple times about focusing on dividends being major component in shareholder return. They even reiterated this during the most recent Q2 2019 earnings call. This is just the type of dividend income company investors should like for the long run.

I received a handful of shares of KTB as part of the VFC spin off. After studying the company, I decided to increase my position. I would add more if I see their financials improving in another 2-3 quarters. Here is my proof of purchase which is also updated in my dividend investing portfolio.

UPDATE

Until February of this year, things looked pretty good on Kontoor Brands. It reached a high of 41.87$ and was giving out dividends. However, the COVID pandemic resulted in them cutting the dividend. Most dividend based etf’s were forced to sell their Kontoor Brands holdings. So we saw the effect of forced selling for dividend cuts this time around. Stock went to as low as 14$. So far I have kept buying despite the cut. Management even spoke about possibility of reinstating dividends in Q4 of 2020 if debt and bank covenants improve by then. Listening to calls management does seem to be working towards reinstating dividends. Not sure when it will happen but I like what they have been saying so far. I also learnt about selling covered calls for income. I did this with my Kontoor Brands stock position and I still own the stock.

Disclaimer: The above are just my opinions expressed in the article. I am not your fiduciary or an investment advisor. Do not consider this as investment advice to you. This article is just for informational and entertainment purposes. Also please note that this article was published on Aug 25th. Many numbers would have changed when you are reading it.

References: